ALL You Need to Know About the Average Car Insurance Cost

Last Updated: July 7, 2022

Insurance is one of those things you don’t think you need…

… until you do.

Car insurance is no exception.

And yet, every time you pay your premium, you’re left wondering:

Am I overpaying for car insurance?

Maybe you are, maybe you are not.

Before we find out, let’s warm up with some recent stats:

- The average car insurance cost is $1,529 per year.

- Louisiana drivers pay $2,226 more per year than New Hampshire drivers.

- At-fault drivers pay $561 more per year on average for their premium after an accident.

- Drivers with very poor credit pay $1,537 more for car insurance than drivers who have exceptional credit.

- Teen drivers pay $3,446 more per year than drivers in their fifties.

- Women pay 0.1% more than men on average.

- Doctors pay 1.2% less than civil servants.

- Uber and Lyft drivers pay 49% more.

- Married people pay 7.3% less on average.

- The average cost of car insurance for SUVs is $1,952 for a six-month premium.

The only way to find out is to compare your rate to the average car insurance cost in your state while taking into account all of the factors that can impact it…

Nevertheless, one of the most important things you need to know is:

What is the average car insurance cost in America?

This will give you a general idea of whether you are overpaying and need to have a chat with your insurance agent, or if you are paying less and should count your lucky stars.

Before we go into all of that, let’s cover some of the basics.

The General Auto Insurance

If you were to ask your friends and family how much each of them is paying for insurance, you will find that the costs vary greatly.

Your married aunt in her fifties is probably paying less for her insurance than your 18-year-old cousin. So what gives?

What factors affect the cost of car insurance?

Naturally, the type of insurance you have will affect the cost — some drivers can only afford the legally required minimum while others opt for more comprehensive coverage.

It goes without saying that getting the bare minimum is also the cheapest option, whereas getting full coverage car insurance is way more expensive.

So, let’s check out those other factors that aren’t as obvious.

Location

Insurance companies factor in your location when determining the rates. For starters, each state has different laws regarding the minimum required coverage.

Then, there are some areas where car accidents are more common. For example, you are more likely to be involved in a fender bender in a city with busy traffic, rather than on a rural country road.

This is one of the reasons why car insurance prices vary greatly by state and even by city.

Driving history

Every insurance company is trying to determine which applicant has a higher chance of getting into an accident which costs them money in damages.

‘High-risk drivers’ usually get a higher rate than those that have never been involved in an accident or gotten a ticket.

That said, most insurance companies will forgive your driving mistakes after 3 to 5 years.

So, make sure to shop around if three years have passed since your last speeding ticket. Who knows, you may find a company that offers you a lower insurance premium.

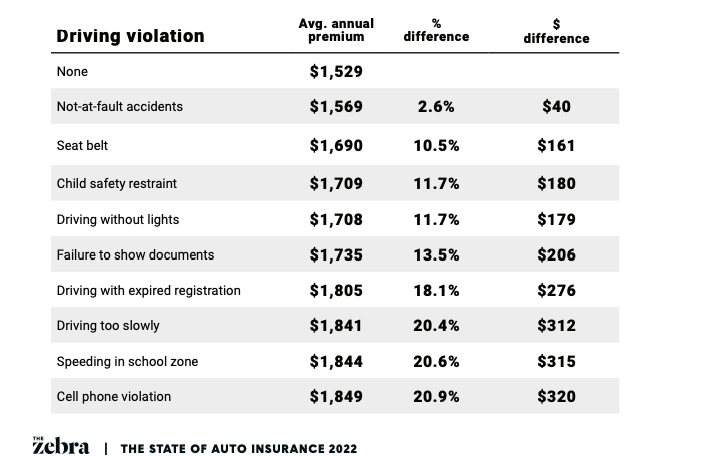

So, how much does car insurance cost for drivers with traffic violations and accidents? The table below illustrates the averages based on the type of road offence.

(Image Source: The Zebra)

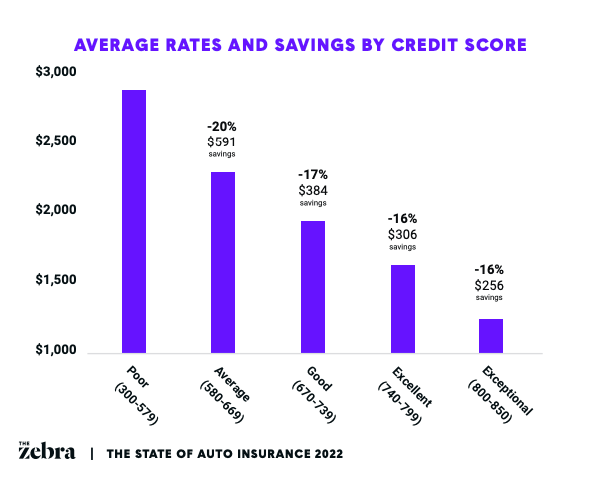

Credit score

Insurance companies are not allowed to use your credit score to determine the costs of your car insurance in four states — California, Hawaii, Massachusetts, Michigan, and Washington. For the rest, your score is fair game.

A 2007 report by the Federal Trade Commission suggests that credit scores have been effective at determining higher-risk consumers.

The main thing that interests insurance providers is whether you have made any recent insurance claims.

It’s important to note, however, that not every company values your scores the same way. If you shop around, you will find that some companies will give you a better rate than others.

Just like with your driving history, if more than 3-5 years have passed since your last credit mishap, you’re free to shop around. Negative information is usually removed from your credit report after 5-7 years.

Check out our article featuring the latest credit score statistics to find out how you compare to the national average, and to get some tips on how to improve your FICO score.

(Image Source: The Zebra)

Age and gender

Yup, the average car insurance rates by age and gender can vary. Teenagers, and more specifically male teens, pay the most.

The reason for this is that male teenagers are statistically more likely to get into an accident than their female counterparts.

Don’t worry, you won’t be paying as much down the line. Drivers in their twenties pay significantly less, and the average car insurance payment goes down as you age.

Those in their fifties have the lowest rates. Your costs may increase slightly as you reach your eighties though.

There you have it — just get older and your rates will decrease.

Unless… you are a woman in your forties. In some states, women have a slightly higher auto insurance rate. The difference is less than 1%, though.

Profession

Naturally, people that use their cars often for work-related purposes will have higher rates. That said, occupation might have an impact even on the rates of those that don’t use their vehicle for work.

Insurance companies associate certain occupations with more-risky behaviour, thus more likely to file claims. Also, some professional organizations work with insurance companies to discount car insurance rates for their members.

Statistics show medical professionals get the cheapest car insurance quotes. They earn an average savings of $19 per six-month auto insurance policy.

Marital status

Ah, the joy of marriage! Lifelong companionship, growing old together, cheap car insurance…

Wait, what?

Yup — married people are considered to be less risky drivers and more financially stable.

Spouses also usually insure both their vehicles at the same company, which means bundle deals. So, perhaps they are getting a discount for multiple car insurance.

Yet, once teenage kids are in the mix, their rates increase.

Divorcees though get higher rates since they are deemed to be riskier drivers.

Vehicle type

Insurance rates vary by car model. Not surprisingly, sports cars are more expensive to insure than SUVs. Also, cars that are cheaper to repair will also give you lower car insurance rates.

Types of Car Insurance

Now that we have gone over what factors affect the cost of your insurance, let’s review the main types of insurance you can get — which also impacts the cost.

We already mentioned that the minimum legally required car insurance is the cheapest option. Let’s explain what that is.

Liability insurance

In almost every state — except New Hampshire and Virginia — drivers are legally required to have this type of insurance.

Why is that so?

The purpose is to have a guarantee that if you cause an accident, or if you are an at-fault driver in an accident, any injuries caused to other drivers, passengers, pedestrians, as well as any damage to property will be covered.

There are two types of liability insurance:

- Bodily injury liability — covers all of the expenses related to injured drivers, pedestrians, and passengers.

- Property damage liability — covers the costs related to any property damage you have caused.

You will usually notice this format:

25/50/25

This means that insurers will cover:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident (applies if you injure multiple drivers, passengers or pedestrians in one accident)

- $25,000 property damage per accident

While getting this type of insurance is mandatory, there are still a lot of uninsured drivers on the road. And sometimes, the required minimum is not enough to cover all of the costs.

Which brings us to:

Uninsured or underinsured motorist coverage

This type of coverage kicks in when you get into an accident with a driver who is at fault, or liable, but either doesn’t have insurance or the insurance they have is not enough to cover all your medical costs or property damage.

Collision insurance

This is a sort of vehicle insurance — the purpose is to cover the costs related to repairing your car.

Let’s say you are the driver who is at fault and you have caused damage to your car. For example, you have hit a lamp post or bumped into another car.

This type of insurance will cover the costs incurred by the traffic collisions you have caused.

Comprehensive insurance

Your car can get damaged without getting into an accident. And this is the reason why people get comprehensive (sometimes called full) coverage.

Naturally, the average cost of full coverage car insurance is higher. It covers any damage caused by:

- Fire

- Hurricanes, tornadoes

- Falling objects

- Animals

- Theft

- Vandalism

So, when do you need comprehensive insurance?

Is it worth it?

It doesn’t make sense to get this type of insurance if you are driving an older car that doesn’t cost much.

The main reason you would want or need this type of insurance is:

- you have a new and expensive car,

- when you are in the middle of a lease pay off or

- in the middle of a loan pay off.

Check out the latest car loan stats to get a general idea of the full vehicle costs!

Car Insurance Rates

What we’ve learned so far is that insurance companies use all sorts of info to predict whether you are a high-risk driver that will cost them money or whether you are a reliable person.

Now, let’s move on to check out some of the national average insurance rates for cars:

- Drivers aged 16-19 pay an average of $4,796 for an annual premium.

- On average, drivers aged 30-39 pay $1,495 for an annual premium.

- The average annual premium after texting while driving is $1,851.

- On average, the annual premium after reckless driving is $2,417.

- The average 6-month car insurance premium after a DUI is $1,324.

- The average annual premium for drivers with very poor credit scores is $2,848.

Compulsory Auto Insurance

Ever since people could afford cars, they started having accidents with them. Along with those came damages and all types of accident-related costs.

There was no way to ensure that the driver who was at fault would be able to pay out those damages, so regulations were put in place.

Massachusetts and Connecticut became the first states where car insurance became compulsory in 1925. Other states followed suit and car insurance became state-regulated.

The pros of compulsory car insurance are:

- It eliminates the risk that at-fault drivers will be unable to pay out damages.

- It can be cheaper than being responsible for covering the damages on your own.

The cons of compulsory car insurance are:

- Not all drivers can afford car insurance.

- Drivers can save money — provided they never get in an accident.

How Much Does Average Car Insurance Cost in my State?

Some states have compulsory car insurance, some don’t.

In New Hampshire for example, you aren’t legally required to have insurance, yet you are still responsible for covering all damages you may cause.

As car insurance is regulated on a state, rather than the federal level, each state has different minimum legal requirements.

This is the reason for the difference in auto insurance rates by state.

It is also the reason why drivers in Michigan pay around 82% more than the national average — personal injury protection (PIP) insurance is legally required.

This entails paying for unlimited medical coverage for accident-related injuries.

The downside is that insurance companies compensate for these costs by increasing the rates.

So there you have it. Costs can vary greatly by state, which is why you get quotes based on your ZIP code.

Now, let’s check out the states with the lowest car insurance average cost.

| State | Average annual premium |

| New Hampshire | $999 |

| Ohio | $1,028 |

| Maine | $1,035 |

| North Carolina | $1,067 |

| Virginia | $1,067 |

| Hawaii | $1,088 |

| Vermont | $1,158 |

| Wisconsin | $1,202 |

| Iowa | $1,218 |

| Washington | $1,224 |

Top 10 states with the most expensive rates for car insurance:

| State | Average annual premium |

| Louisiana | $3,265 |

| Michigan | $2,639 |

| Florida | $2,425 |

| Rhode Island | $2,106 |

| Kentucky | $1,879 |

| California | $1,810 |

| Nevada | $1,768 |

| Arkansas | $1,768 |

| Missouri | $1,698 |

| Colorado | $1,687 |

Cheap Car Insurance

By now you have probably figured out that the best way to determine the cost of your insurance, is to talk to an insurance broker or agent.

Everything from your driving history to your age and location can affect the cost — some factors more than others.

Some insurance companies will only slightly increase your rates if you’ve been caught texting while driving, while others will bump up your premium.

Then there are those that don’t care much about your credit history and those that judge you for your high credit utilization rate.

Naturally, we all strive to reduce our costs whenever we can.

After all, the latest consumer spending stats show that transportation costs are no joke.

Yet, no one will advise you to skimp out on car insurance. The more comprehensive your coverage is, the better.

And this is why it is recommended to compare auto insurance quotes for the same coverage. Just to get a general idea of which company offers a lower rate.

That said, there are some insurers that offer affordable coverage options.

These are some of the companies that offer cheap car insurance policy options for a minimum required coverage of six months:

- Nationwide – $541

- GEICO – $562

- Progressive – $627

- USAA — $636

- State Farm – $646

- Farmers – $787

- Liberty Mutual – $863

- Allstate – $1,019

And how much is car insurance monthly with these companies?

- Nationwide – $90

- GEICO – $94

- Progressive – $104

- USAA — $106

- State Farm – $108

- Farmers – $131

- Liberty Mutual – $144

- Allstate – $170

Note: when you do your car insurance comparison, keep in mind that USAA is only available to military members, veterans, and eligible family members.

How to Save on Car Insurance?

There are things you can change and then there are things that are out of your control.

Both of these affect your insurance costs, but at least there is some hope of improving the rates you get.

So, how to get cheaper car insurance?

For starters, have you tried not being a teenager?

Jokes aside, here are some ways in which you can save some money on car insurance.

1. Shop around.

Look into the various insurance policies offered. Get a quote from multiple companies and compare them. You can never know which one has the best car insurance rate for you.

2. Bundle your insurance.

We are going to assume that your car isn’t the only thing you are insuring. Bundling all of your different policies for a better rate can also result in car insurance savings. See if you can get health insurance, home insurance, life insurance and auto insurance at the same company.

3. Improve your credit score.

There isn’t a quick fix for anything. But, if you manage to pay your bills on time and have a credit utilization ratio of around 30%, you will improve your score over time.

4. Raise your deductible.

By doing this, your out-of-pocket costs will be higher when you make a claim. However, it is a sure way to reduce your premium for car insurance.

5. Check if you qualify for a discount.

Some companies offer car insurance discounts for drivers with low mileage, drivers who have installed safety features in their cars, good students, and drivers who pay for six-month or yearly insurance at once.

Car Insurance Cost Calculator

Wondering how much your car insurance will cost?

No worries, we’ve got you covered (pun intended).

Here are some cost calculators you can use to check your average auto insurance cost:

- GEICO Coverage Calculator

- StateFarm Car Insurance Quote

- Liberty Mutual Quote

- Progressive Car Insurance Estimator

- Allstate Car Insurance Quote

- Erie Insurance Quote

- Amica Auto Quote

After getting a quote from multiple companies, you may find that the car insurance estimates are somewhat similar. Or not! This is why research is essential!

Key Takeaways

You are now aware of all of the pricing factors when it comes to car insurance. So, how to get cheap car insurance?

Let’s sum things up:

- Car insurance is state-regulated and the legally required minimum insurance determines the minimum price.

- If you want the lowest car insurance prices, you can get the minimum coverage.

- Only do this if you don’t have any assets to protect.

- You can lower your auto insurance premium by driving safe, improving your credit score, bundling your insurance and raising your deductible.

- Compare quotes from multiple companies to find out which has the cheapest rate.

Let’s not forget the best trick there is for lowering your costs:

Get married and be in your fifties.

Insurance companies will hate you.

And that is all there is to know about the average car insurance cost.

FAQ

Yes, you need auto insurance to drive a car in the US. Minimum coverage requirements vary by state. Only New Hampshire and Virginia don’t have mandatory car insurance laws. However, if you choose not to purchase a policy, you must pay an extra fee each year, along with your vehicle registration. Also, in case of a car accident, you need to cover the associated costs.

The average insurance cost per month is $128 as of 2022. But there is a significant difference between the cheapest and the most expensive car insurance. Some companies offer rates starting at $90 a month, while certain factors can bring up the cost to over $400 a month.

For example, if you’re a teen driving Maserati in Louisiana (lucky you), prepare to pay a monthly premium equal to a six-month coverage plan for a Honda owner in their fifties, living in New Hampshire.

There’s no set cost for adding another person to your car insurance. It all depends on the secondary driver’s profile and the insurer.

For example, adding a teen to your policy will increase your annual premium by 102%, on average. Meanwhile, adding a 30-year-old driver with no traffic violation history will cost just 13% extra.

As of 2022, the average car insurance cost per year is $1,529. But there are many variables determining the price, including the type of coverage, your age and gender, state of residence, marital status, profession, credit score, traffic violations history, and vehicle model.

ABOUT AUTHOR

After I got my degree in translation and interpreting, I started working in a typical office. To get away from my nine-to-five job, I ventured into freelance writing. One thing led to another, and I ended up creating content for SpendMeNot. I have been involved with this site ever since its launch — first as a writer and now as a manager.