Income Needed to Buy a House

Last Updated: January 11, 2023

What is Our Information Based On?

The Property Market in the US

Do I Qualify for A Home Loan?

How Much Mortgage Can I Afford?

A Simple Exercise to See if You Have the Salary Needed to Buy A House

How Much Money Should I Save Before Buying A House?

How to Qualify for a Mortgage in Terms of Your FICO Score

What is a Good Fico Score?

How Can I Improve My FICO Score?

What Does It Take to Buy A House?

The Priciest States to Live In

Conclusion

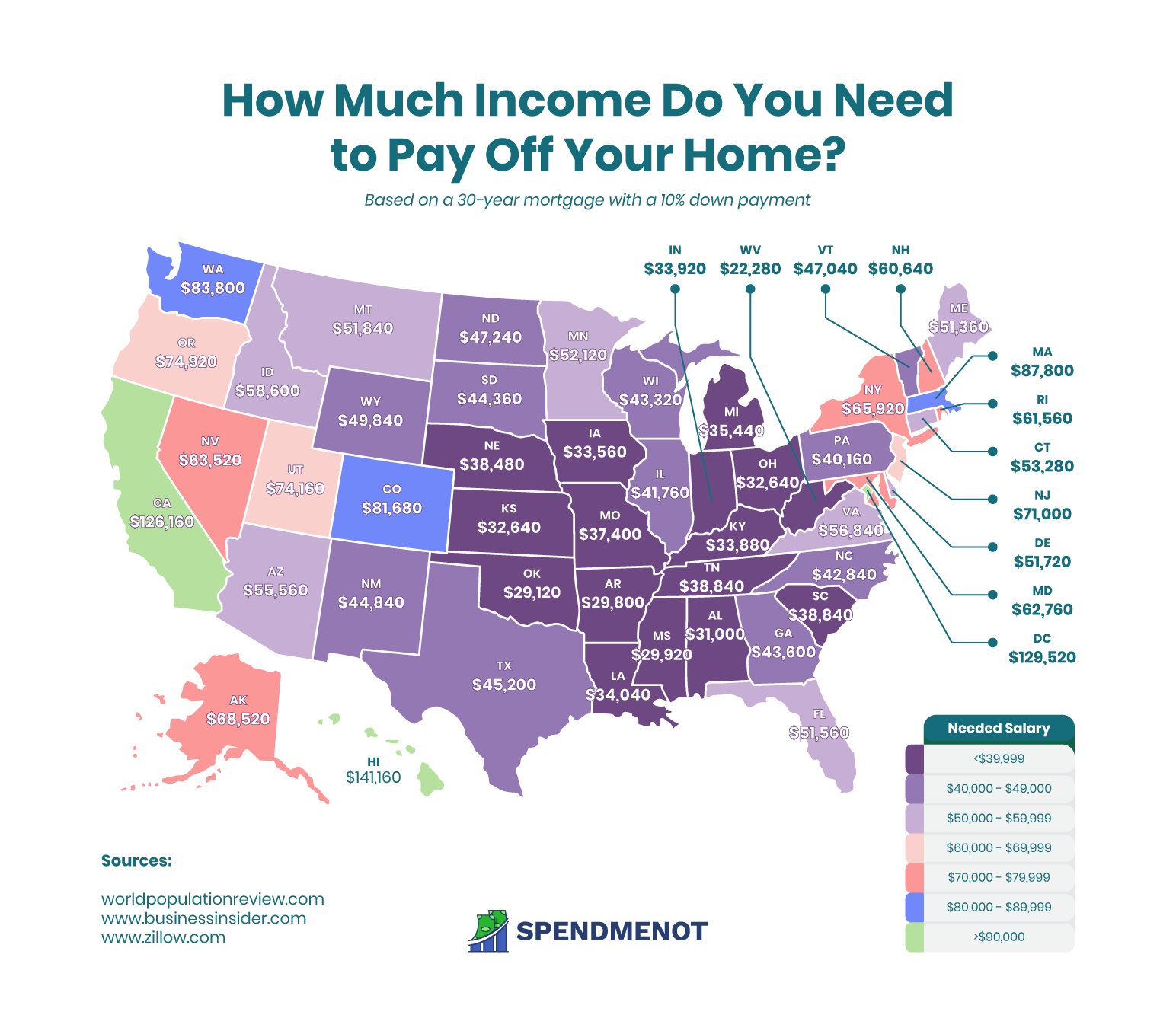

What’s the income needed to buy a house across the US?

Should you save for a deposit?

Is it a good idea to save for a deposit first?

First things first.

This Map Shows the Income Needed to Buy a House

Here is our slick, detailed, one-of-a-kind map showing the amount of money you need to buy a house based on the state you live in.

We also have a list of the most expensive locations to own a house, but more on that later. For now, let’s cover the basics.

Are you ready to enter the property market?

Can you afford to?

In this post, we’ll answer all of those questions and a lot more besides.

We’ll go through the top twenty states in the US, detailing:

- Average Home Value

- Monthly Payment

- Monthly Salary Needed

We’ll also go through factors that affect the property market in each state.

Let’s get started:

What is Our Information Based On?

There are many options when it comes to home loans in the US. We’ve based our calculations on standard mortgage payments over a 30-year term. We’ve assumed that all homeowners have a deposit of 10%.

We’ve also assumed that they’ve got the income required for mortgage maintenance and that they had a fair to good credit rating.

The Property Market in the US

The property market in the United States is relatively stable. The average value of a home is currently $231 000. Property values over the last year rose by 4.8% and are expected to rise by another 2.8% over the next twelve months.

The total number of units in the US is 138.45 million. Of that, 57% are owner-occupied. 31% are rented out. The remaining 13% are either under construction or currently vacant.

The housing market was extremely strong until subprime lending caused the market to take a dive. Part of the problem was that banks were granting higher risk loans. They also became less strict on qualifying factors such as the minimum income to buy a home and credit-worthiness.

This, in turn, triggered a global recession in property markets. The markets have been recovering slowly, but we’re still nowhere close to pre-2007 levels of optimism.

The homeownership rate in the United States amounted to 64.8% in 2018. The homeownership rate is the proportion of households which are occupied by the owners. This reached its peak in 2004 before the 2007-2009 recession hit and decimated the housing market. The rate continued to fall until 2016 but has begun to increase again since then.

Qualifying criteria such as the income requirements for a home loan vary from state to state. The average mortgage interest rate is 3.66%. We do need to note, though, that each person is awarded a rate based on the amount of risk they pose. That’s why we recommend checking factors like your FICO score before considering buying a home.

Do I Qualify for A Home Loan?

Each financial institution has its own set of criteria to work with. In general, though, to qualify for a home loan, the following basic criteria must be met. You must:

- Provide proof of your income and identity.

- Not pay more than about a third of your salary on your bond.

- Have a fair to good credit rating.

- Be permanently employed.

How Much Mortgage Can I Afford?

To work this out, divide your take-home pay after taxes by three. Work on the salary that you’re earning now and don’t factor in increases that you might earn later. If you’re thinking, “It’ll be a little difficult until I get my increase,” then you can’t really afford the loan.

In addition to the third of your salary, you must also make allowances for sundry expenses. These include dues, insurance, maintenance, and taxes. Keep in mind that as the owner of the property, you’ll be liable for all of these costs.

In answer to the question, “How much salary do I need to buy a house?” there are few minimums in place. The bank will consider your application on its merits. Again, they’ll usually suggest that the repayment is under 33% of what you and your partner earn after taxes.

You don’t want to exceed this by much, if at all. A bond is a serious commitment, and you just don’t know what will happen down the line. What if there’s an emergency? If the majority of your salary is going to repaying a mortgage, that doesn’t leave you with much of a safety cushion to work with.

Also, should the rate or expenses increase during the term, could your mortgage repayment prove overwhelming?

A Simple Exercise to See if You Have the Salary Needed to Buy A House

This exercise might not be that popular because it requires patience. But it is highly effective and can help you qualify for a better rate. So, the six months that it takes will be well-spent.

Start by creating a savings account for your deposit. Now work out how much your installment would be monthly. Add in extra for insurance and maintenance. Now take that total, and deduct the amount that you’re paying for rental at the moment.

Now comes the critical part. Put the remaining money into your savings account. Do this every month. Why? What better way to prove that you do have the income needed to buy a house? If you’re able to manage this savings program, you prove to the bank and yourself that you can afford it.

Not only that, but you’ll also have a nice lump sum to use as a deposit.

How Much Money Should I Save Before Buying A House?

You should ideally have a deposit of at least 10% of the purchase price, but the more you can put aside upfront, the better. If you have an excellent FICO score, the bank might allow you to buy without a deposit.

Just keep in mind that there is a range of costs to consider. Having the property registered in your name is something you have to hire a conveyancer for. This can be pretty expensive. If you have nothing saved, you’ll have to pay these fees out of pocket. Unless the property value is significantly higher than the asking price, the banks won’t allow you to include this fee in the bond.

If your credit rating is low, you might be asked for a more substantial deposit. It’s also worth noting that the higher the deposit is, the less risk you pose to the bank. They’ll give you a better rate as a result.

How to Qualify for a Mortgage in Terms of Your FICO Score

We spoke a little earlier about your FICO score. A FICO score is an indication of how well you manage your debt. Odd as it may seem, too little debt is just as bad as too much debt. If you have no debt at all, the banks have no way to tell if you’re a good payer or not.

If you’ve got a bad score, they’ll know you’re not, so you won’t get the loan. When you decide to buy a home, check your FICO score first. If it’s on the low side, it’s pointless to ask how much money do you need to buy a house. Even if you do qualify in terms of income, you’ll pay a higher interest rate.

Now, an extra 0.5% on loan doesn’t sound like a lot. But we’re talking about a large sum of money being repaid over a thirty-year term. Let’s use an example to demonstrate how expensive that can be.

We’ll assume that you’re buying for $100 000. We’ll further assume that you’ve got a $10 000 deposit. Let’s take a look at that calculation at a rate of 3%.

The repayment would be $379 per month, without interest or other incidentals. That means that over the term, you’d pay back a total of $136 440.

Now let’s increase that interest to 3.5%. The repayment would be $404, without interest and other incidentals. Doesn’t sound like much of a difference, does it? Except that here you’ll be paying a total of $145 440. That’s an extra $9 040.

But it doesn’t stop there. The worse your credit rating, the more you’ll pay for insurance as well. All of this affects the answer to the question, “How much income to buy a house?”

What is a Good Fico Score?

- If you have a score of over 810, you’re all set. This is an excellent rating and will secure you the best rates on interest and insurance.

- 750-809 is considered great.

- 670-749 is considered good.

- 560-669 is considered fair. You may still get a mortgage in this category, but the interest rates will be higher.

- 500-559 is considered poor. If you’re at the upper end of this range, you might get a partial loan, but the interest rates will be high.

- Anything below 500 is considered bad credit. You will not get a loan from a reputable lender.

If you’re unsure of the answer to “How much mortgage can I qualify for?” speak to your bankers about getting a preapproval. They’ll be able to tell you exactly where you stand.

How Can I Improve My FICO Score?

Even if you have terrible credit, you can improve things significantly in six months. You have to:

- Pay your debt on time every month.

- Reduce your overall debt by paying down credit accounts. Ideally, you should never use more than 50% of your credit limits on all accounts.

- Reduce the total number of accounts. Even if you pay your accounts down, those open credit limits could be problematic. Why? Because you still have access to that credit. Pay down some accounts and close them. Do leave a credit card and a store account open so that you can prove that you’re good at paying your accounts on time.

What Does It Take to Buy A House?

Buying a home involves a lot of paperwork, but you don’t have to do much running around. You’ll find a home that you like and make an offer. We recommend making the offer contingent on getting an 80% or 90% mortgage. That way, if the bank says that they’ll lend up to 60%, you have a legal out.

Once the seller accepts the offer, it goes into escrow. You’ll need to come up with the money for the transfer and stamp duty if it’s not included in the loan amount.

The Priciest States to Live In

And now that we know all the basics, let’s dive right in with the specific facts and figures.

1. Hawaii

(Source: Zillow)

- Average Home Value: $614 800

- Monthly Payment: $3 529

- Monthly Salary Needed: $11 763

How much income do you need to buy a home in Hawaii? If you want to move to Hawaii, you better start saving sooner rather than later. It ranks at the top of our list in terms of salary required. There are some less expensive properties on the island, but you should earn at least $11 760 a month to put you on a good footing.

What’s more, Maui County has also been named amongst the most expensive counties in the US. You’ll need to consider where the house is placed. Is it in an active lava zone? If so, financing is hard to come by. Zone 9 areas are those that have had no eruptions in 60 000 years.

The 30-year mortgage rate, at 6.69%, stayed the same for November 2019.

2. Washington, DC

(Source: Zillow)

- Average Home Value: $563 400

- Monthly Payment: $3 238

- Monthly Salary Needed: $10 793

Properties here are pricey. But then again, Washington, DC is known as the top state to get paid.

There are many high-value homes in the area, with some selling for as much as a whopping $15 million. According to experts, there are still housing opportunities. But finding the right deal might mean tempering your expectations. If you’re patient, you might even get lucky.

The 30-year mortgage rate dropped from 3.63% to 3.62% in November 2019.

3. California

(Source: Zillow)

- Average Home Value: $548 600

- Monthly Payment: $3 154

- Monthly Salary Needed: $10 513

California is known as the state with the most billionaires.

Sunny California has one of the largest property markets in the country. How much should you make to buy a house in California? That depends on where you buy, but bank on at least $10 000 a month. Demand is high, particularly in San Francisco, San Jose, San Francisco, and San Diego. Property in larger cities tends to sell fast. If you see a great deal, snap it up before someone else does.

4. Massachusetts

(Source: Zillow)

- Average Home Value: $407 400

- Monthly Payment: $2 195

- Monthly Salary Needed: $7 316

The property market in Massachusetts has been growing from strength to strength. Demand is fast outstripping supply, pushing housing prices up. Home loan qualifications are fairly strict in the Pilgrim State, so make sure you’ve got your finances in good order before applying.

At 3.6%, the 30-year mortgage rate stayed the same in November 2019.

5. Washington

(Source: Zillow)

- Average Home Value: $388 400

- Monthly Payment: $2 095

- Monthly Salary Needed: $6 983

The Evergreen State is also experiencing an upswing in the property market, with the cost of living higher than the national average. The cost of properties makes a significant contribution to this higher cost of living. The Seattle metro area is the most popular area in the state, which has an effect on the salary needed to buy a house.

The 30-year mortgage rate dropped from 3.68% to 3.59% in November 2019.

6. Colorado

(Source: Zillow)

- Average Home Value: $378 300

- Monthly Payment: $2 042

- Monthly Salary Needed: $6 806

Colorado’s property market has been healthy over the last few years. Experts expected the bubble to burst, but it looks as though they were wrong. The lifestyle and great economic situation in the state are highly attractive to prospective buyers.

The 30-year mortgage rate dropped from 3.63% to 3.65% in November 2019.

7. Oregon

(Source: Zillow)

- Average Home Value: $346 300

- Monthly Payment: $1 873

- Monthly Salary Needed: $6 243

How much money should you have to buy a house in Oregon? You’re looking at around $300 000 in the bigger cities. The Beaver State’s housing market has been growing rapidly over the last few years. In 2015, home values averaged out at $239 000. They have since increased by almost 6%. And that’s not all – research indicates that the property market will grow more.

That said, it is slowing. For now, though, it’s still very much a buyer’s market.

The 30-year mortgage rate, at 3.65%, stayed the same in November 2019.

8. New Jersey

(Source: Zillow)

- Average Home Value: $327 800

- Monthly Payment: $1 775

- Monthly Salary Needed: $5 916

This is another area where there has been decent growth over the last few years. It hasn’t been steady growth, though. Between 2015 and 2019, average property values increased by as much as 16.58%. That being said, demand for homes is relatively stable. The percentage of new homes built since 2000 is just 11.3%, which indicates that supply is on an even keel. The Garden State has the highest property taxes in the US.

The 30-year mortgage rate increased from 3.65% to 3.70% in November 2019.

9. Alaska

(Source: Zillow)

- Average Home Value: $315 900

- Monthly Payment: $1 713

- Monthly Salary Needed: $5 710

Alaska’s economy has been in recession since 2015. What’s interesting about this is that it hasn’t impacted the income needed to buy a house. Normally, we’d expect to see house prices drop. What we do see, though, is that the prices are stable. So, there’s no huge growth in this state, but there are also no big drops in property value.

The 30-year mortgage rate, at 3.60%, stayed the same in November 2019.

10. New York

(Source: Zillow)

- Average Home Value: $303 600

- Monthly Payment: $1 648

- Monthly Salary Needed: $5 493

In recent months, the media has reported that the New York property market is in “freefall.” This may have caused some panic, but experts agree that this is oversimplifying the case. In fact, experts have been predicting an adjustment in property prices since the close of 2015.

The property market was at a high in 2015. It was inevitable that the bubble would burst. And now that it has, it’s a good time for those wanting to buy property and take advantage of the slightly lower income needed to buy a house.

The 30-year mortgage rate dropped from 4.43% to 4.41% in November 2019.

11. Nevada

(Source: Zillow)

- Average Home Value: $292 300

- Monthly Payment: $1 588

- Monthly Salary Needed: $5 293

How much salary do I need to buy a house in Nevada? That depends on where you buy. Property prices in Las Vegas are steep. Property values in Nevada have increased by 64.34% over the last five years. A third of the homes in the state were built after 2000. This is thanks to increasing demand and decreasing supply. Looking at the statistics over the last five years, it’s clear that the market is starting to reach peak maturity. So, an adjustment in values is imminent.

At 3.66%, the 30-year mortgage rate stayed the same in November 2019.

12. Maryland

(Source: Zillow)

- Average Home Value: $288 700

- Monthly Payment: $1 569

- Monthly Salary Needed: $5 230

Property values in Maryland are relatively stable. The overall values have only appreciated by 17.6% since 2015. Properties in the state sell relatively quickly, showing that there is plenty of demand. The state has more than enough properties for investors. The market is strengthening and in the beginning stages of an upswing. The answer to the question, “How much do you need to make to buy a house?” is a lot less than in many other states.

The 30-year mortgage rate dropped from 3.58% to 3.56% in November 2019.

13. Rhode Island

(Source: Zillow)

- Average Home Value: $283 000

- Monthly Payment: $1 539

- Monthly Salary Needed: $5 130

Rhode Island is facing a housing crisis. It’s not that there aren’t enough properties, but rather that those properties are not affordable for most. There’s been an upsurge in interest in starter homes, possibly in response to high housing prices. That said, it is hard for a low-income family to afford their own home here. Make sure you have the base salary needed to buy a house before making an offer.

The 30-year mortgage rate, at 3.65%, stayed the same in November 2019.

14. New Hampshire

(Source: Zillow)

- Average Home Value: $278 700

- Monthly Payment: $1 516

- Monthly Salary Needed: $5 053

Property values have appreciated by 29.03% over the last five years. Property taxes in New Hampshire are the third-highest in the country. The property market is strong, and the demand for houses is high. The state is attractive for investors – the crime rates are lower, and the unemployment rate is better than average.

The 30-year mortgage rate, at 3.63%, stayed the same in November 2019.

15. Idaho

(Source: Zillow)

- Average Home Value: $268 900

- Monthly Payment: $1 465

- Monthly Salary Needed: $4 883

Property values in the state have appreciated by 55.57% over the last five years. The property market is strong. Around about a quarter of the houses were built after 2000, indicating that supply is limited. How much income is needed to buy a house in Idaho? We’d say work on a figure of at least $4 000.

The 30-year mortgage rate, at 3.57%, stayed the same in November 2019.

16. Virginia

(Source: Zillow)

- Average Home Value: $260 700

- Monthly Payment: $1 421

- Monthly Salary Needed: $4 736

Property values in Virginia have appreciated by 19.4% over the last five years. About a fifth of the houses have been built since 2000. The housing market is active, and there is a great deal of demand for suitable properties. Virginia is an affordable alternative when it comes to the income needed to buy a house.

The 30-year mortgage rate dropped from 3.68% to 3.66% in November 2019.

17. Arizona

(Source: Zillow)

- Average Home Value: $254 600

- Monthly Payment: $1 389

- Monthly Salary Needed: $4 630

Property values have appreciated by 42.87% since 2015. About a third of all homes have been built since 2000. The market here is subject to fluctuations, and so development is something of a stop-start affair. The reason for these fluctuations is changes in population.

The 30-year mortgage rate, at 3.77%, stayed the same in November 2019.

18. Connecticut

(Source: Zillow)

- Average Home Value: $243 800

- Monthly Payment: $1 332

- Monthly Salary Needed: $4 440

Property values have appreciated by 8.6% over the last five years. New homes built since 2000 constitute just 8.5% of the statistics. This is because the Constitution State is one of the smallest and most developed states. How much do I need to make to buy a house in Connecticut? Close to $4500 a month.

The 30-year mortgage rate, at 3.59%, stayed the same in November 2019.

19. Minnesota

(Source: Zillow)

- Average Home Value: $238 300

- Monthly Payment: $1 303

- Monthly Salary Needed: $4 343

Property values have appreciated by a massive 29.59%. The Minneapolis-St Paul metropolitan area is the most popular in the state. Property prices there are high as a result. The property market is robust, and properties don’t take long to sell on average. How much income do I need to buy a house in Minnesota? Minnesota is one of the most affordable options on our list, coming in at under $5 000.

The 30-year mortgage rate dropped from 3.64% to 3.61% in November 2019.

20. Montana

(Source: Zillow)

- Average Home Value: $236 900

- Monthly Payment: $1 296

- Monthly Salary Needed: $4 320

Property values have appreciated by 28.79% in the last five years. Appreciation over the last ten years is 27% and also amongst the highest in the country. Around about a fifth of homes in the county was built since 2000.

The 30-year mortgage rate, at 3.62%, stayed the same in November 2019.

Conclusion

Hopefully, you’ve found our list informative. We’ve tried to answer common questions like,“How much should I save to buy a house?” and give you solid advice on how to improve your credit score. If there’s one lesson that you take away from this, though, we hope it’s that property purchases shouldn’t be rushed into.

Now, this can be difficult when you’re all excited about getting your own place. It might seem silly to wait. But, if you’ve got a poor credit rating or not quite enough for a deposit, it would be better to wait.

Here’s the bottom line:

There’s a lot more to mortgage finance than just ensuring that you have the income needed to buy a house. The consequences of making a bad decision here are serious. If you default on your mortgage, your home will be repossessed. And adverse listings related to bonds stay in the system for up to 30 years. With that in mind, it pays to be more careful here.

Sources

ABOUT AUTHOR

Fiona worked in the retail banking industry for 16 years. She felt that she could put her experience to good use in helping small businesses grow. Web writing was a great fit and sparked a new career for her. She believes that her flexible working schedule gives her more time to spend painting. She loves being at home all day with her schnauzers and her cat. For Fiona, it's furbaby Friday every day of the week.