21+ Cash vs Credit Card Spending Statistics to Know in 2023

Last Updated: March 10, 2023

Cash or credit card?

Which is better?

The latest cash vs credit card spending statistics will shed some light on the matter!

Cash vs Credit Card Spending Statistics (Editor’s Pick):

- Almost 60% of consumers prefer using cards.

- Americans have 3.84 credit cards on average.

- Cash represents 19% of all transactions in the US.

- 80% of cash transactions are for payments under $25.

- 46% of consumers use a cashback card.

- People are willing to spend up to 100% more when using a credit card.

- Americans make 23 debit card payments in a typical month.

The majority of us have wallets filled with too many cards and a bit too little cash…

Unless you are one of those people that uses cash for everything.

Now:

How many Americans use credit cards?

Nearly 200 million adults in America have credit cards.

Yup!

We have many more impressive facts to share. But first, let’s talk about:

Types of Payment Methods

Before we move on to the global payment industry overview and compare the usage of cards, it seems suitable to explain the most commonly used payment methods.

They are:

- Cash

- Credit Cards

- Debit Cards

- Electronic Payment Systems

- Mobile Wallets

Cash is pretty self-explanatory. It’s the Benjamins, the Jackson bills… or, if you’re lucky, you may be one of the rare owners of the discontinued 500 notes.

Besides having a jar full of coins in your car and hopefully a lot of Benjamins in your wallet, you probably own a few cards.

Not every card is the same, though.

Let’s start with the credit card definition.

When you are using a credit card, you are basically borrowing money from the bank. The bank determines your credit card limit. This is the maximum amount you’re allowed to spend.

Well, you can spend more, but your bank will get mad. In fact, exceeding your limit or getting near your limit can hurt your credit score. The credit card utilization rate is an important factor when it comes to calculating your score.

Don’t believe us? These credit score statistics prove it.

Now, where were we? Ah, yes. Credit cards.

At the end of each month, you need to pay your credit card bill in full – and settle all of your debts. If you do – then you won’t get charged interest.

However, if you carry your credit card balance into the next month, you will get charged interest on the unpaid balance. If you fail to keep up with payments and your rates are not favorable, you may find yourself in high-interest debt.

By paying off your credit card balance fully and on time, you may get rewards. So, yeah – you can make money by spending money… responsibly!

Now:

What is the main difference between a credit card and a debit card?

Before we move on to the credit and debit card usage statistics, we should clarify what sets them apart.

So, when using a credit card, you’re borrowing money from the bank to pay for goods and services. Then, you’re paying the loan off at the end of the month.

And when you’re using a debit card, you’re using money that you own. The money comes from your bank account – it could be money you deposited, saved, or earned.

Moving on:

PayPal is the best example of an electronic payment system for online money transfers.

(If you’re looking for more information on PayPal statistics, this is your chance.)

And then, a mobile wallet. This is basically a virtual, online wallet that stores your card info. You can use it at stores that have a digital payment terminal.

Cash vs Credit Card Spending Statistics

Now that we have explained the different types of payment methods, let’s get to the statistics:

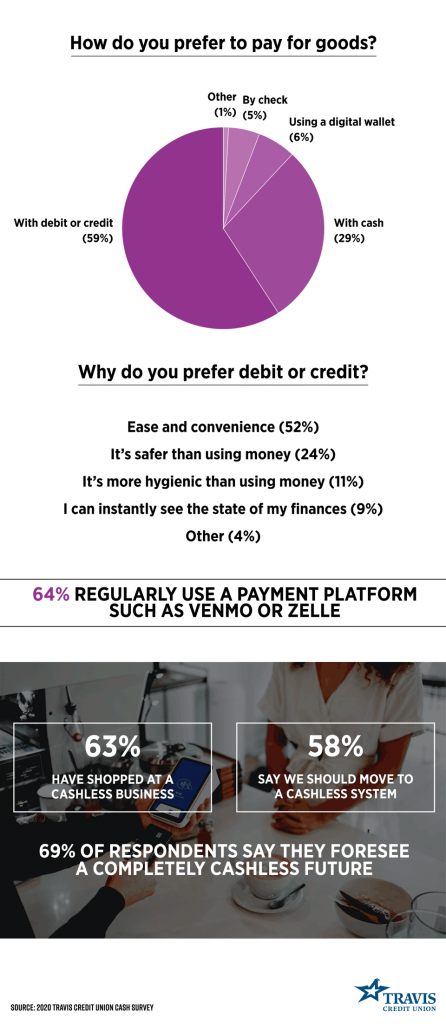

1. 59% of US consumers prefer using payment cards.

(Source: Travis Credit Union)

According to Travis Credit Union’s 2020 survey data, Americans’ most preferred payment method is debit or credit card. Only 29% of consumers favor cash.

What’s more, people were asked why they prefer using credit and debit cards. More than half (54%) of the survey respondents cited the ease and convenience of this payment method. In the picture below, you can see the other reasons stated.

(Image Source: Travis Credit Union)

2. Debit cards accounted for 28% of all payments in 2020.

(Source: Federal Reserve Bank of San Francisco)

Apparently, debit cards are the most used payment method.

According to payment method statistics, credit cards represented 27% of all transactions, while cash accounted for 19% of the total.

3. On average, Americans make 23 debit card payments per month.

(Source: Federal Reserve Bank of Atlanta)

In a typical month in 2020, consumers, on average, made 18 credit or charge transactions and 14 cash payments. They also wrote 3 checks and made 8 direct bank transfers.

4. Credit cards are the most preferred payment method in the Northwest.

(Source: Finder)

Credit card statistics from 2020 show that credit cards narrowly beat out the use of a debit card in the Northeast as a preferred payment option by 30.51% of consumers.

Also, roughly 30% of respondents from either coastline — West and Northeast — prefer to use credit cards, whereas closer to 20% of those from the Midwest or South chose that payment method.

Meanwhile, debit cards are the most preferred payment method among consumers in the:

- West — 35.57%

- South — 38.35%

- Midwest — 37.30%

5. Just 16% of Americans always carry cash.

(Source: Travis Credit Union)

As evidence of the society evolving towards a cashless future and the growing global digital payments market, just 16% of survey respondents stated they always had bills in their wallets. Some 27% said they carry cash most of the time, while 37% responded ‘sometimes.’

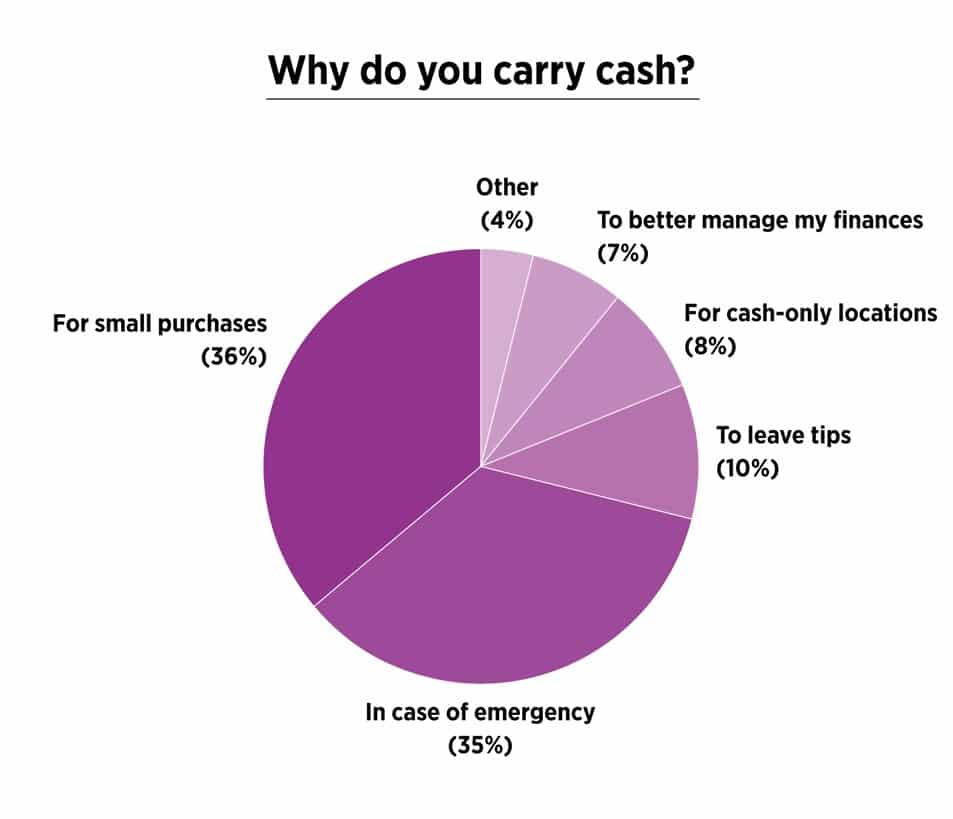

6. Americans carry an average of $46 in cash.

(Source: Travis Credit Union)

The main reasons Americans carry cash is for small purchases and in case of emergency. Interestingly, while just 7% said they do it to manage their finances better, a vast majority of respondents (62%) admitted they are less likely to overspending when paying in cash.

(Image Source: Travis Credit Union)

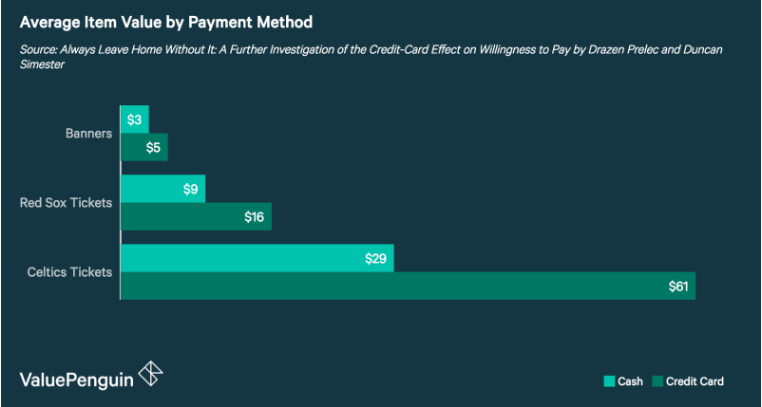

7. Consumers are willing to spend up to 100% more when using a credit card.

(Source: MIT)

As noted in the previous entry, some people carry cash to avoid overspending. Indeed, cash vs credit card spending statistics prove people spend more money when paying with credit cards.

As stated in the study ‘Always Leave Home Without It’, participants were willing to spend up to 100% more when paying with a credit card!

One group was required to pay with cash and the other with a credit card. However, both groups needed to pay by 5 p.m. the next day. Tickets to a sold-out game were auctioned, and the participants had to write down their bids.

The participants who had to use a credit card were more prone to overpaying.

Here is the average amount both groups were willing to spend:

(Image Source: Value Penguin)

8. Cash transactions declined by 7 percentage points in 2020.

(Source: Federal Reserve Bank of San Francisco)

Recent credit card and debit card transaction volume statistics show cashless payments are becoming the norm, and you may be wondering:

What percentage of transactions are in cash?

The 2021 Diary of Consumer Payment Choice has found that cash payments represented 19% of all transactions in the US in 2020. This was 7 percentage points down from 2019. So, there is a significant decline in the use of cash in the USA.

9. Small-value cash payments decreased by 26% in 2020.

(Source: Federal Reserve Bank of San Francisco)

This explains the decline in the use of cash.

Why?

Well, cash is mainly used for small-value purchases, global payment reports show. In the US, 80% of all cash transactions are for goods and services below $25. Also, some 50% of payments under $10 are in cash.

Have you ever noticed how stores have cash discounts or credit card minimums?

This is because merchants need to pay a processing fee to card networks such as American Express.

For example, the store needs to pay 3% of each transaction to the card network. And instead of paying the processing fee, some stores decide to offer a cash discount.

The dollar amount spent in cash vs. credit transactions is, in general, smaller for the former payment method and higher for the latter.

10. Cash reigns in the South.

(Source: Finder)

A cashless society?

That’s a ‘NO” from 20% of people in the South.

Those in the Midwest are not too far behind at 17.48%. These regions are followed by the Northeast and the West, where cash is the preferred payment method for 15.81% and 14.29% of people, respectively.

11. As of June 2, 2021, there was cash worth $2.17 trillion in circulation in the US.

(Source: Federal Reserve)

Although the global digital payments market is growing, the amount of US cash in circulation is increasing.

Just check out the total US currency in circulation by year:

- 2020 – $1.87 trillion

- 2019 – $1.79 trillion

- 2018 – $1.67 trillion

- 2017 – $1.57 trillion

- 2016 – $1.46 trillion

- 2015 – $1.38 trillion

- 2014 – $1.3 trillion

- 2013 – $1.2 trillion

- 2012 – $1.13 trillion

- 2011 – $1.03 trillion

- 2010 – $0.94 trillion

- 2009 – $0.89 trillion

- 2008 – $0.85 trillion

- 2007 – $0.79 trillion

- 2006 – $0.78 trillion

- 2005 – $0.76 trillion

12. There were 653 million VISA debit cards in the US in 2020.

(Source: Statista)

Debit card usage statistics show there were approximately 653 million VISA debit cards in the second quarter of 2020 in the US alone. Worldwide, there are more than 2.3 billion!

13. There were 250 million debit or prepaid MasterCards in the US in 2020.

(Source: Statista)

In the third quarter of 2020, there were 250 million MasterCard debit cards in the US alone. Worldwide, excluding the US, there were 1.08 billion cards.

14. The number of VISA credit cards in circulation in the US was 343 million in 2020.

(Source: Statista)

According to credit card usage statistics, more than 1.14 billion VISA credit cards are in circulation worldwide. Out of these, more than 798 million are outside the USA.

15. The number of MasterCard credit cards in circulation in the US was 246 million in 2020.

(Source: Statista)

Worldwide, there were 967 million MasterCard credit cards in circulation in 2020. Some 721 million were outside the US.

16. 79% of Americans own at least one credit card.

(Source: Federal Reserve Bank of Atlanta)

The 2020 estimate is the highest since the Fed began conducting the Survey of Consumer Payment Choice in 2008.

Here are some other credit card usage statistics by country:

- Israel – 75.10%

- Canada – 73.10%

- Luxembourg – 62.70%

- Hong Kong – 59.30%

- New Zealand – 58.30%

- Australia – 56.30%

- United Kingdom – 55.30%

- Norway – 54.20%

- South Korea – 53.90%

17. Americans hold an average of 3.84 credit cards.

(Source: Experian)

US credit card usage statistics show that most people have multiple cards.

The 2020 figure is down 4% from the previous year. Experian explains the decline with a pattern of US consumers shedding credit card debt as the coronavirus pandemic spread financial uncertainty.

New Jersey citizens held the highest average number of credit cards — 4.54. At the other end of the spectrum was Alaska, with 3.06 cards per person.

And here are some credit card usage statistics by age:

- Gen Z — 1.91 credit cards on average

- Millennials — 3.18 credit cards on average

- Gen X — 4.23 credit cards on average

- Baby Boomers — 4.61 credit cards on average

- Silent Generation — 3.64 credit cards on average

18. 46% of US consumers use a cashback card.

(Source: The Ascent)

The most commonly owned types of credit cards are cashback and store credit cards.

Now:

How do cashback credit cards work?

Every time you use your card, you get a certain amount back. So, let’s say you have spent $1,000 this month. If you get 1% back, then you have ‘earned’ $10.

And:

How do store credit cards work?

Most store credit cards can only be used with the specific retailer only, though there are some open-loop credit cards. If you are using a store card, you may be eligible for many discounts within that store.

However, if you don’t frequent the store often, there is no point in getting one. In general, with store credit cards, users have lower credit limits while also paying high rates of interest.

(Image Source: The Ascent)

19. The average credit card debt per person is $5,313.

(Source: Value Penguin)

The average American has a credit card balance of $5,313 and a credit score of 710. And in terms of credit card utilization rate, on average, people use 25.3% of their credit card limits.

20. 62% of consumers adopted at least one payment app in 2020.

(Source: Federal Reserve Bank of Atlanta)

The global digital payments market is growing at a steady pace. The adoption of online payment platforms increased by 8% in 2020, reaching 62% of consumers.

The top companies in the payment market were PayPal (42%), Venomo (24%), and the bank-account-linked Zelle (17%).

21. The global digital payments market is expected to reach $132.5 billion by 2025.

(Source: PR Newswire)

First, let’s start with the definition of digital payment. Digital payments can be defined as transactions that are made digitally, over the internet, or through a mobile channel. We’re all familiar with card payments and EWallet payments, which are good examples.

Digital payments reports estimate that the market share will reach $132.5 billion at a compound annual growth rate (CAGR) of 17.6% over the next six years. This can be attributed to the growing demand for fast and secure transactions, as well as the increased growth rate in China and India.

22. The global payments market size is estimated to reach $2 trillion by 2025.

(Source: PR Newswire)

As stated in the Valuates report on the market size, status, and 2018-2025 forecast on global payments, the market size will have a CAGR of 7.83%. The market of mobile online payments based on near-field communication (NFC) is growing fast.

Some important payments market analysis and trends featured in the report are:

- The first region to perform more than 50% of transactions electronically is North America.

- The Asia-Pacific region accounts for almost half of the global payments revenue.

- In Latin America, the payments market has been the fastest-growing industry.

Some of the top companies in the payment market are:

Which Payment Method is Best?

Wondering which payment method is best for you?

Let’s compare the use of cash vs. credit vs. debit.

Credit Card Fraud, Stolen Money and Identity

Credit card fraud is not something to be taken lightly. According to the latest credit card fraud statistics, Americans lose billions of dollars each year due to fraud.

However, if your credit card gets stolen, you do have some level of protection. Once you notice that the card has been stolen, you need to contact the card issuer. If you report that your card has been stolen before a fraudulent charge has been made, then you won’t be liable for the charges. In other words – you won’t have anything stolen from you.

If a charge has been made after you reported that your credit card had been stolen, then you will be liable for up to $50.

Of course, If you lose cash, then it is probably gone for good. Maybe that’s one of the reasons for the decline in the use of cash. The only silver lining here is that you aren’t at risk for a stolen identity or credit card fraud.

And what about an ATM or debit card? If you report the theft within two days, you will be liable for $50. After two days, you can be liable for $500. And if you don’t notice that your debit card has been stolen after 60 days, then you will lose all the money taken from your account.

Perks and Rewards

Some types of credit cards feature various perks and rewards. You can rack up points and get a cashback, discount, or a special offer by using the card frequently. But don’t let this fool you! The cashback you get is usually a small percentage of the purchase.

Fees

Credit card membership fees are usually higher than debit card membership fees.

It really is a never-ending cycle of surcharges and fees:

- Annual fee,

- Late fee,

- Balance transfer fee,

- Foreign transaction fee,

- Card replacement fee,

- Over limit fee,

- Finance charge…

And if you carry your balance over the next month, you will be paying high rates of interest. This is a common mistake credit users make. They usually only pay the minimum payment and then end up stuck with high-interest debt.

As for cash… well there are no fees. Only the ATM charges!

Cash Withdrawal

And speaking of ATMs, did we mention the cash advance fee?

When you need to draw from the line of credit the bank has lent you, you also need to pay the cash advance fee.

So it’s definitely cheaper to withdraw cash using a debit card or an ATM card.

Damaging Your Credit Score

This is one of the disadvantages of credit cards that need to be discussed before you get one. Each missed or late payment and the amount of credit debt you have will cause credit damage that is hard to undo.

Not impossible, but still.

It takes years to build good credit and just a few months to ruin it. If you don’t have a stable income, then a debit card may be a better option for you.

Improving Your Credit Score

If you’re one of those who avoids banks like the plague and prefers to pay with cash for everything… then don’t be surprised when the banks turn your back on you when you come begging for a loan.

To get a loan, you need to have a credit history. The longer you have had the account — the more points you get for having a credit history.

Emergency Expenses

The ability to pay for emergency expenses is not one of the features of debit cards. It’s rather a subject of cash vs credit transactions debate.

If an emergency expense occurs that you cannot afford, you can use your credit card and pay the money back later. But if you’re only using cash or a debit card and don’t have any savings, you will find yourself in a tough financial situation.

A word of advice: Don’t use your credit card for nonessential purchases you can’t afford. For example, upgrading your phone. Do use it if your car breaks down and you don’t have another mode of transport.

Ultimately, using a credit card responsibly can improve your finances.

Disputing Charges

If you pay for something with cash and a debit card and are not satisfied with the service or the goods are damaged, it’s up to the merchant whether you will receive a refund.

But if you used a credit card, then you can call your bank and dispute the charge. This is another one of the benefits to cardholders.

Accepted Payment Methods

Not every merchant accepts cards, and sometimes paying with cash isn’t possible – as is the case when buying something online.

So it’s best to carry both cash and cards with you. The cashless society may be growing, but there is still a need to have some bucks with you. Just in case, you know.

Online Shopping

While cash is mostly used for in-store purchases, you need to have at least one card that you can use for your online purchases.

According to online payment statistics, there are millions of active users of online payment platforms. Even if we aren’t close to a cashless society, digital payments are widespread.

Currency Conversion

If you’re traveling in a country that uses another currency, you can still use your card. However, make sure you check what the currency conversion fees are.

Exchanging cash for local currency is better if you’re traveling in a place where cards aren’t used often.

Key Takeaways

Getting to know all the credit card advantages and disadvantages will help you make a more informed decision on when to use a card and when to pay with cash.

Both credit and debit cards are convenient — provided that you use them responsibly. If you don’t trust your financial decisions, stick with cash for everyday purchases.

Cash vs credit card spending statistics prove that a combination of various payment methods is the only way not to be limited in your purchases.

Spend responsibly!

See you around on SpendMeNot, guys.

Sources

ABOUT AUTHOR

After I got my degree in translation and interpreting, I started working in a typical office. To get away from my nine-to-five job, I ventured into freelance writing. One thing led to another, and I ended up creating content for SpendMeNot. I have been involved with this site ever since its launch — first as a writer and now as a manager.